Charting Encryption Pathways That Secure Recurring Revenue Streams in Multi-Channel Retail Setups

Retail operations that rely on recurring revenue often span online stores, physical locations, and mobile applications, which creates multiple points where payment data moves between systems. Encryption serves as the mechanism that protects card details and subscription information during these transfers while supporting consistent billing cycles. Industry reports indicate that tokenization combined with transport layer security protocols allows merchants to replace primary account numbers with unique tokens that merchants store instead of raw card data.

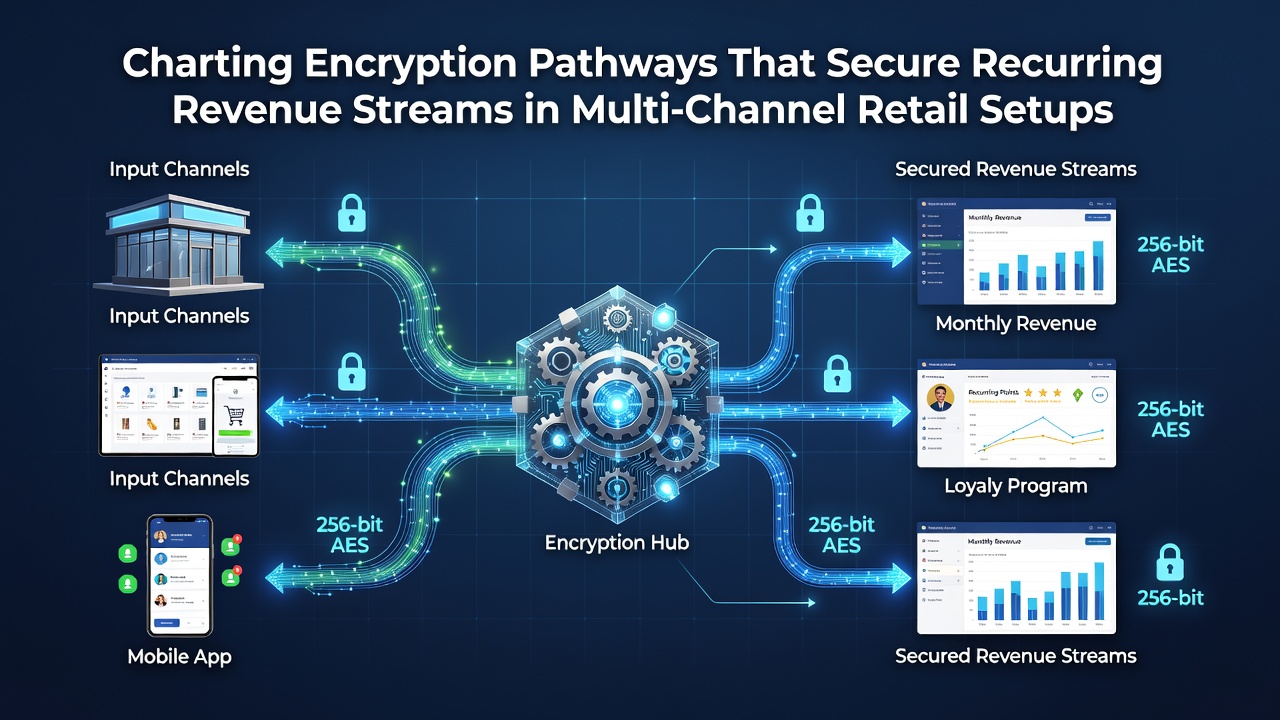

Those who manage multi-channel setups frequently map encryption pathways from the point of capture through authorization and settlement. Data shows that AES-256 remains the standard for protecting stored information at rest, whereas TLS 1.3 handles encryption during transmission. Researchers at institutions such as the National Institute of Standards and Technology have documented how key rotation schedules reduce exposure windows when keys are updated every ninety days in high-volume environments.

Core Components of Encryption Pathways

Pathways begin at the device level where point-of-sale terminals or web forms collect payment credentials. End-to-end encryption then wraps the data so that only the payment processor holds the decryption keys. Observers note that this separation prevents retail staff or internal systems from accessing full card numbers even during routine processing. Tokenization follows immediately after initial capture, generating a reference that subscription platforms use for subsequent billing without re-entering sensitive details.

Key management systems coordinate these steps across channels. Hardware security modules store master keys in tamper-resistant environments, and software agents distribute session keys to individual applications. Figures from payment networks reveal that merchants who centralize key management across all channels experience fewer discrepancies during reconciliation processes that occur at the end of each billing cycle.

Supporting Recurring Revenue Across Channels

Subscription models require repeated authorization without repeated collection of full credentials. Encryption pathways enable this by linking tokenized records to customer profiles that update automatically when payment methods expire. In June 2026, several payment gateways introduced enhanced token lifecycle management features that automatically refresh tokens before expiration dates, reducing involuntary churn rates documented in merchant surveys.

Multi-channel consistency demands that the same token format works whether a customer initiates a subscription through a mobile app, a website checkout, or an in-store kiosk. Application programming interfaces enforce uniform encryption standards so that a token generated on one channel remains valid on others. Studies from European payment research groups indicate that this interoperability cuts integration time by approximately thirty percent when new channels are added to existing retail networks.

Security Standards and Regulatory Alignment

PCI DSS requirements specify encryption controls that apply equally to recurring and one-time transactions. Merchants must demonstrate that cardholder data remains encrypted during storage and transmission, with documented procedures for key custody. Compliance audits examine whether pathways maintain separation between encryption and decryption functions across all retail touchpoints.

Regional regulations add further layers. The Australian Prudential Regulation Authority has issued guidance on data protection for financial services that includes recurring payment streams, while Canadian provincial privacy statutes require explicit consent mechanisms tied to encrypted storage practices. Merchants operating internationally often adopt the strictest standard across jurisdictions to simplify audit processes.

Emerging Techniques and Implementation Patterns

Homomorphic encryption appears in pilot programs that allow computations on encrypted data without decryption, which could eventually let analytics teams examine subscription trends while keeping raw payment information protected. Early adopters report that current performance overhead remains significant, yet laboratory tests continue to narrow the gap between encrypted and plaintext processing speeds.

Zero-trust architectures now influence how pathways are segmented. Each channel operates as an independent zone that must re-authenticate before accessing shared token vaults. Network segmentation logs show that this approach limits lateral movement if one channel experiences a breach, thereby protecting the broader recurring revenue pool.

Conclusion

Encryption pathways that connect capture points, token vaults, and authorization systems form the backbone of secure recurring revenue operations in multi-channel retail. Standards such as AES-256 and TLS 1.3, along with centralized key management, provide measurable protection that scales across online, physical, and mobile environments. Continued alignment with PCI DSS and regional regulations ensures these pathways remain both functional and compliant as new channels and techniques emerge.