Currency Conversion Protocols and Fraud Monitoring in Subscription-Based Merchant Platforms

Subscription-based merchant platforms process recurring payments across multiple currencies every day, and currency conversion protocols sit at the center of both revenue accuracy and risk detection. These protocols handle exchange rate calculations, apply markups where required, and route transactions through compliant channels while feeding data directly into fraud monitoring systems that scan for anomalies in real time.

How Conversion Protocols Operate in Recurring Billing

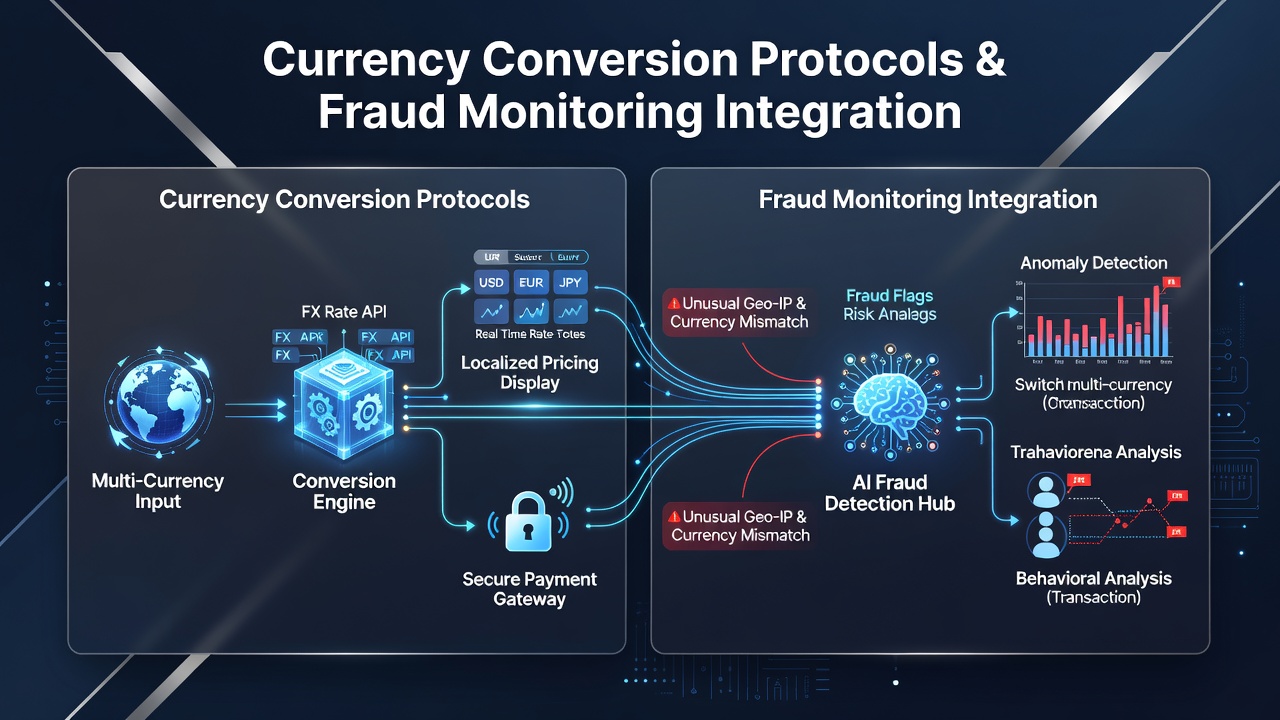

Merchants set up subscription accounts with defined billing cycles, and platforms apply conversion rules at each renewal because customers often hold cards issued in different currencies. The process begins when the merchant submits a transaction in the billing currency, after which the acquiring bank or processor retrieves the current interbank rate, applies any agreed spread, and converts the amount before authorization reaches the card network. Systems record every rate snapshot along with timestamps and merchant identifiers, creating an audit trail that later supports both reconciliation and fraud analysis.

Dynamic currency conversion offers cardholders the choice to pay in their home currency at the point of sale or during checkout, yet subscription platforms typically default to the merchant's base currency to maintain consistent pricing. Protocols must therefore distinguish between one-time DCC selections and standing instructions for recurring charges, and they log these distinctions because deviations from expected patterns can trigger review queues in the fraud engine.

Linking Conversion Data to Fraud Detection Layers

Fraud monitoring tools ingest conversion metadata alongside standard transaction fields such as amount, frequency, and device fingerprint. When a subscription payment suddenly converts at a rate that deviates more than two standard deviations from the historical average for that merchant-currency pair, the system flags the event for further scrutiny. Analysts note that coordinated testing of stolen cards often involves rapid switches between issuing currencies to probe velocity limits, and conversion logs help surface these attempts because the timing and rate combinations rarely match legitimate subscriber behavior.

Platforms also compare conversion outcomes against geolocation data from the cardholder's device. A payment initiated from one country yet converted through an unexpected corridor raises an alert because such routing sometimes indicates money mule activity or account takeover. In June 2026 several processors updated their rule sets to incorporate real-time central bank reference rates as an additional benchmark, allowing faster identification of rate manipulation attempts that previously slipped through static thresholds.

Regulatory Frameworks Shaping Both Conversion and Monitoring

Payment service directives in the European Union require transparent disclosure of conversion margins on recurring billing statements, and those same disclosures feed compliance reports that regulators cross-reference with fraud incident data. In Canada the Office of the Superintendent of Financial Institutions expects acquirers to maintain documented procedures for rate validation, procedures that overlap with anti-money laundering transaction monitoring obligations. Observers note that these overlapping requirements push platforms to build unified data pipelines where conversion events and fraud signals share the same storage layer, reducing latency between detection and response.

One processor that serves subscription software companies implemented a correlation engine in early 2025 linking daily exchange rate volatility reports to chargeback ratios. The model revealed that currency pairs experiencing sudden spreads above 1.8 percent coincided with elevated disputes thirty days later, prompting the addition of interim authorization holds when volatility thresholds were crossed. Data from the Federal Reserve's 2025 payments report showed similar patterns across North American processors, confirming the value of tying conversion telemetry to downstream risk metrics.

Technical Integration Patterns Observed Across Platforms

Modern subscription gateways expose APIs that return both the converted amount and a risk score calculated from conversion metadata. The score incorporates factors such as historical merchant volume in that currency, time-of-day rate stability, and proximity of the card's issuing country to the merchant's primary market. When the score exceeds internal thresholds teh platform can route the transaction through stepped-up authentication or queue it for manual review without interrupting the subscription renewal flow for low-risk accounts.

Batch reconciliation processes run nightly and compare actual settlement amounts against the conversion values recorded at authorization time. Discrepancies beyond tolerance levels generate exception reports that fraud teams review because settlement mismatches sometimes accompany account takeover schemes that alter card details mid-cycle. Researchers at the Bank for International Settlements have documented how such mismatches appear in aggregate statistics when cross-border subscription fraud volumes rise, providing macro-level validation for the micro-level controls platforms deploy.

Conclusion

Currency conversion protocols generate structured data that fraud monitoring systems rely upon to identify irregular patterns in subscription payments. As processors refine their integration of real-time rates, volatility signals, and regulatory benchmarks, the connection between accurate conversion handling and effective risk detection continues to strengthen. Platforms that maintain synchronized pipelines between these functions position themselves to meet both operational and compliance demands in an increasingly multi-currency subscription environment.