How Support Protocols Shape Underwriting Standards in Multi-Currency Merchant Setups

Multi-currency merchant setups require merchants to accept payments across different currencies while managing exchange rate fluctuations, regulatory compliance in multiple jurisdictions, and varying fraud patterns that emerge in cross-border flows, and support protocols play a central role in feeding real-time data into the underwriting process that determines approval thresholds and risk tiers.

Core Mechanics of Multi-Currency Underwriting

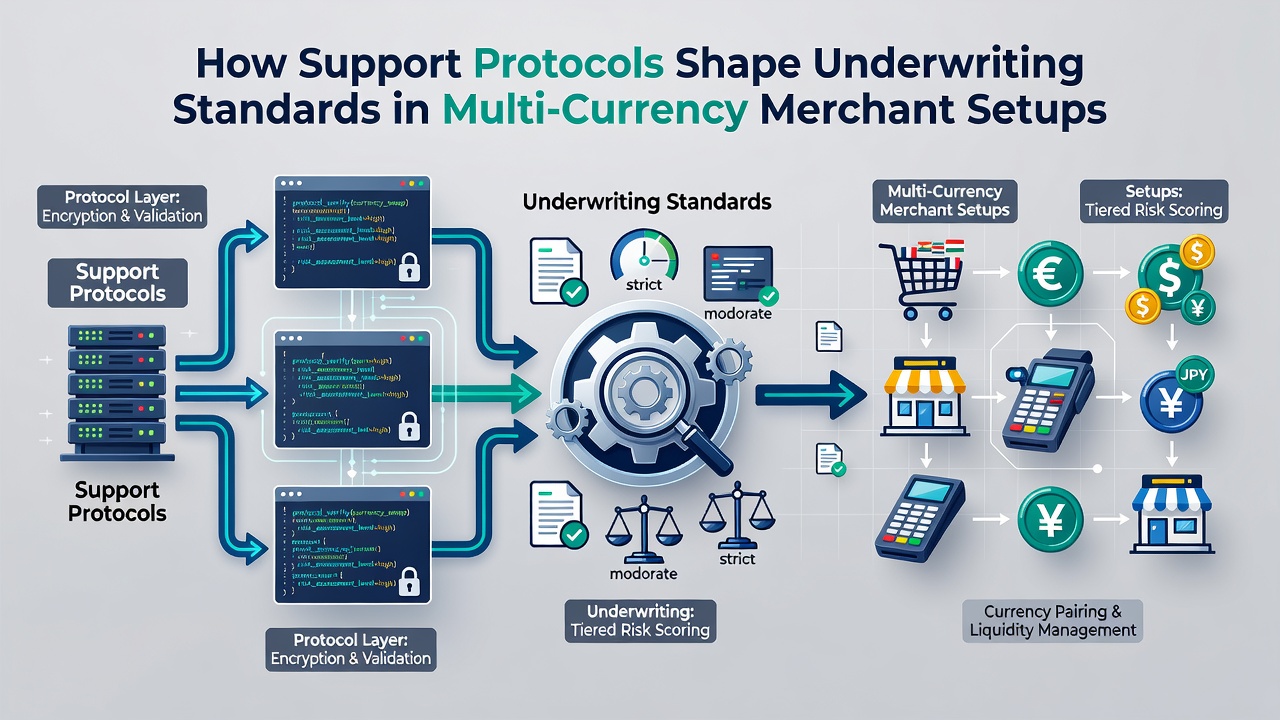

Underwriters evaluate merchant applications by assessing transaction volume projections, historical chargeback rates, and currency conversion costs, yet the quality of incoming support data directly influences how these variables get weighted in the final risk score. Protocols that log every customer interaction, from initial onboarding queries to ongoing dispute resolutions, create datasets that reveal patterns in merchant behavior across currency pairs, and these patterns allow underwriting teams to adjust exposure limits more precisely than volume forecasts alone would permit.

Support Data Streams and Risk Calibration

Support teams document verification steps, currency-specific complaint trends, and settlement delays, then route summarized findings to underwriting platforms where algorithms recalibrate approval criteria on a rolling basis. When a merchant operating in EUR and JPY shows repeated support tickets around delayed settlements, underwriters often tighten reserve requirements or impose higher monitoring thresholds to offset the observed liquidity risk, and this feedback loop has become standard practice among processors handling multi-currency volumes.

Research from the Bank for International Settlements indicates that institutions incorporating support-derived metrics into underwriting models report measurable reductions in unexpected loss events across currency corridors. The integration happens through structured fields that capture interaction outcomes, allowing quantitative comparison against baseline industry benchmarks.

Protocol Design Elements That Influence Standards

Structured escalation paths within support systems ensure that high-severity issues reach underwriting review within defined timeframes, while automated tagging of currency-related queries accelerates pattern detection. These design choices determine whether underwriters receive granular signals or aggregated summaries, and the difference affects how quickly standards evolve in response to emerging risks in specific currency pairs.

Training modules that equip support staff to capture currency context during every interaction further strengthen the data pipeline, because incomplete records reduce the reliability of downstream underwriting adjustments. Observers note that processors with comprehensive protocol documentation maintain more consistent standards even when market volatility spikes in particular regions.

Regulatory Context and June 2026 Developments

European Central Bank guidelines on payment service provider risk management emphasize the need for documented support processes that inform credit decisions, and updates scheduled for implementation around June 2026 are expected to require explicit linkage between interaction logs and underwriting parameter changes. Processors operating across multiple currencies have already begun mapping their current protocols against these forthcoming requirements to avoid compliance gaps.

Similar expectations appear in guidance issued by the Monetary Authority of Singapore, where multi-currency operations fall under enhanced scrutiny for cross-border settlement risks. Support protocols that systematically record regulatory query handling provide the evidence underwriters need to demonstrate alignment with these standards.

Practical Implementation Across Merchant Portfolios

One mid-sized processor handling merchants in USD, GBP, and AUD currencies adjusted its underwriting matrix after support data revealed elevated inquiry volumes around weekend settlement timing in certain time zones, and the resulting changes included differentiated hold periods based on currency and merchant support history. Such adjustments occur incrementally as aggregated support metrics accumulate, allowing standards to reflect operational realities rather than theoretical risk models alone.

Those managing larger portfolios often segment underwriting rules by currency corridor precisely because support protocols surface corridor-specific friction points that generic models overlook. The process relies on consistent data capture rather than ad-hoc reporting, which maintains comparability across different merchant segments.

Conclusion

Support protocols function as continuous input channels that refine underwriting standards in multi-currency merchant environments by supplying empirical evidence of operational and compliance risks that static application data cannot capture, and this relationship has become embedded in both internal risk frameworks and emerging regulatory expectations. Processors that maintain detailed, currency-aware support documentation position themselves to sustain accurate underwriting decisions as market conditions shift across regions and time zones.