Navigating Underwriting Thresholds That Determine Access to Layered Fraud Tools in Subscription Hardware Networks

Payment processors evaluate merchant applications through underwriting thresholds that set the bar for accessing advanced fraud detection systems in subscription hardware environments, and these criteria shape how recurring billing platforms protect against unauthorized transactions across connected devices. Thresholds typically incorporate metrics such as transaction volume projections, historical chargeback rates, and business stability indicators, while subscription hardware networks add complexity because devices often transmit payment data continuously through embedded terminals or IoT modules.

Core Components of Underwriting Thresholds

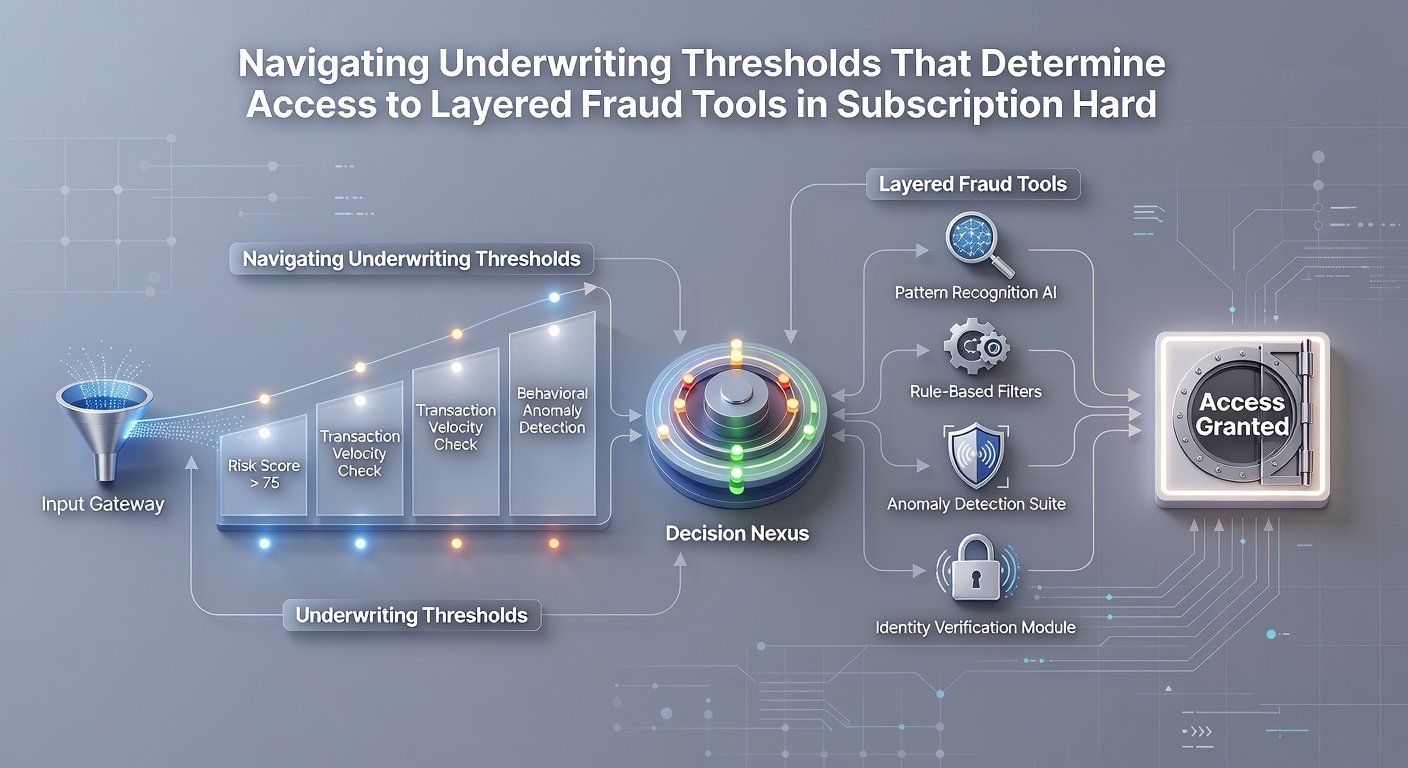

Underwriters assess several data points before granting tiered access to fraud tools, and volume forecasts combined with industry classification determine initial approval levels according to reports from the European Central Bank. Hardware subscription models require additional scrutiny because recurring charges introduce predictable patterns that fraudsters can exploit through account takeover attempts or synthetic identities. Observers note that processors often segment thresholds into low, medium, and high categories, each unlocking distinct layers of machine learning models, velocity checks, and device fingerprinting protocols.

Business longevity plays a central role since newer entrants face stricter reviews compared with established operators who demonstrate consistent compliance records over multiple billing cycles. Data from industry analyses show that merchants exceeding specified chargeback ratios lose eligibility for premium fraud layers until remediation occurs through adjusted pricing structures or enhanced monitoring protocols.

Layered Fraud Tools and Their Access Mechanisms

Subscription hardware networks integrate fraud prevention in stacked configurations where basic address verification sits beneath advanced behavioral analytics and real-time device authentication modules. Access to upper layers depends on clearing underwriting benchmarks that processors update periodically, and these benchmarks reflect aggregate loss data across similar merchant portfolios. When thresholds align with risk appetite parameters, providers activate additional controls such as tokenization for recurring payments and geo-location cross-referencing for hardware terminals deployed in multiple regions.

Processors calibrate these layers using historical patterns from similar deployments, and research from academic institutions indicates that hardware-specific signals like firmware integrity checks improve detection rates when combined with transaction monitoring. Merchants who meet medium-tier thresholds gain entry to velocity monitoring across device fleets while those reaching high tiers receive custom rulesets tailored to subscription renewal dates and hardware lifecycle events.

Regional Variations and Regulatory Influences

Requirements differ across jurisdictions because regulatory frameworks in Canada emphasize consumer protection disclosures during underwriting whereas Australian guidelines focus on data localization for fraud analytics platforms. Processors operating global subscription hardware networks must reconcile these differences when setting unified thresholds that still permit localized tool activation. As of May 2026, updated standards from the Australian Securities and Investments Commission are scheduled to influence how cross-border hardware subscriptions handle threshold recalibrations following new reporting mandates on recurring payment disputes.

One study from the University of Melbourne examined payment flows in IoT subscription services and found that stricter device authentication thresholds reduced synthetic fraud incidents by measurable margins across tested networks. Processors incorporate such findings when refining access criteria, creating feedback loops that adjust underwriting models based on real-world performance data from hardware deployments.

Practical Navigation Strategies Observed in the Field

Merchants preparing applications compile detailed documentation on expected hardware distribution patterns and anticipated renewal rates, and this preparation helps demonstrate alignment with processor risk parameters. Those who have cleared initial thresholds often discover that ongoing monitoring of device health metrics and billing consistency supports retention of higher fraud tool tiers. Take one logistics company deploying subscription-based tracking hardware that maintained eligibility for advanced layers by submitting quarterly device utilization reports showing stable transaction patterns.

Threshold navigation becomes particularly relevant when scaling fleets because volume spikes can trigger automatic reviews that either expand or restrict tool access depending on accompanying risk indicators. Processors communicate these adjustments through portal dashboards that display current standing relative to each underwriting metric.

Conclusion

Underwriting thresholds function as gatekeepers that calibrate fraud tool availability within subscription hardware networks, and successful navigation relies on consistent performance across volume, compliance, and operational stability metrics. Regional regulatory developments scheduled for 2026 will likely introduce further calibration points that processors integrate into existing evaluation frameworks. Organizations that maintain transparent reporting on hardware performance and billing integrity position themselves to retain access to layered protections as network scales expand.