Synergies Among Account Validation Steps That Elevate Detection Layers in Multi-National Terminal Networks

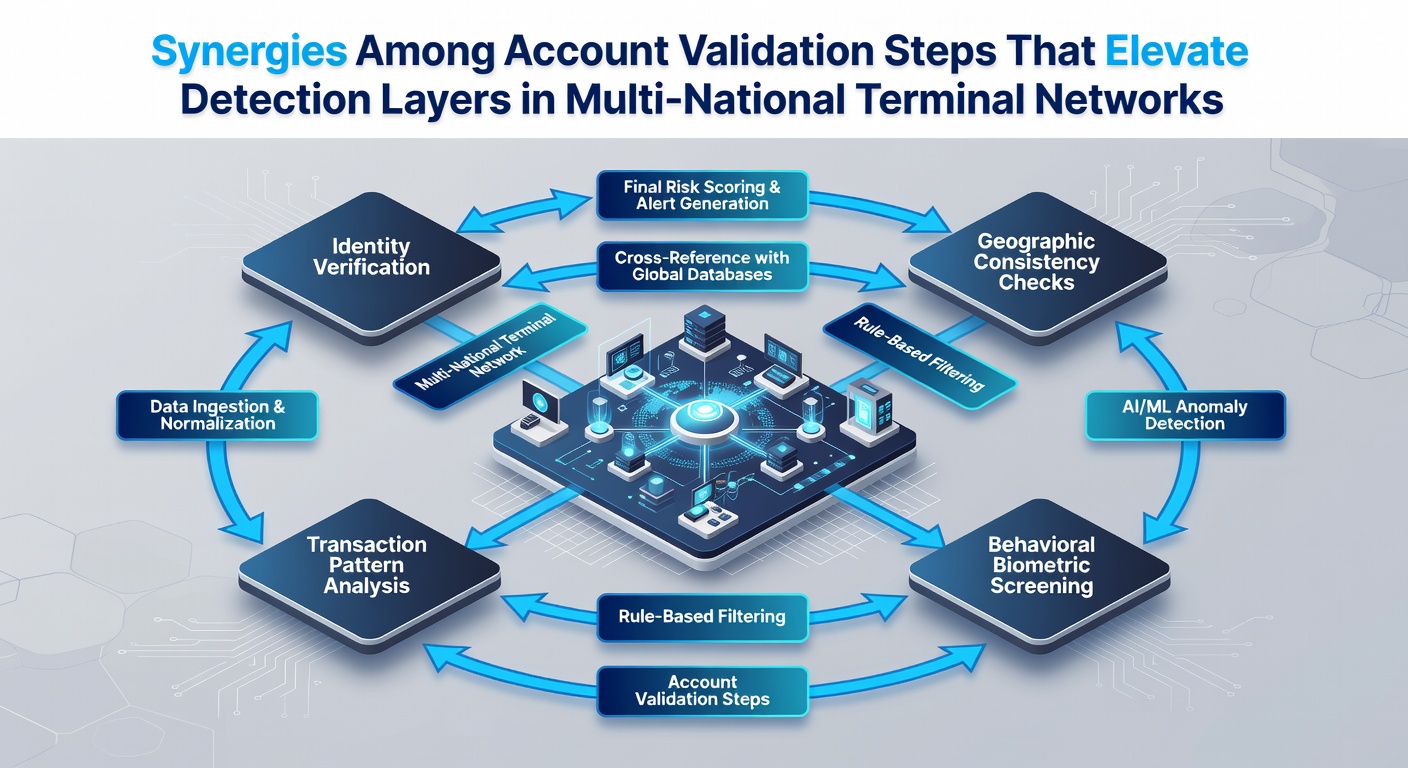

Account validation in multi-national terminal networks combines multiple checkpoints that interact to strengthen overall fraud detection, and operators coordinate these steps across borders where transaction volumes continue to rise through 2026. Systems integrate address verification with card verification values while device fingerprinting adds another dimension that cross-references user behavior patterns recorded at point-of-sale devices in different regions. Data flows between these layers create feedback loops that allow each validation method to refine the others in real time, which researchers tracking payment ecosystems have documented through aggregated transaction logs from networks spanning North America, Europe, and Asia-Pacific corridors.

Core Validation Components and Their Interconnections

Basic account validation begins with primary checks such as card number format verification and expiration date confirmation, yet these steps gain effectiveness when paired with secondary controls like CVV entry and AVS matching that pull from issuer databases located in multiple jurisdictions. Terminal operators configure workflows so that a mismatch in one field triggers deeper scrutiny in another, and this coordination reduces false positives while maintaining throughput at high-volume locations. Studies from payment infrastructure analyses show that networks applying these layered checks in sequence achieve measurable declines in unauthorized attempts compared with isolated verification methods alone.

Device identification tokens collected at the terminal level merge with behavioral analytics drawn from prior sessions, creating a composite profile that travels with the transaction record. When a terminal in one country detects an anomaly in spending velocity, it can reference historical patterns stored from terminals elsewhere, and this cross-border data exchange operates under standardized protocols that preserve privacy requirements while enabling rapid alerts. Observers note that such linkages become particularly relevant as transaction volumes are projected to expand further by June 2026, driven by increased adoption of contactless and mobile-initiated payments across diverse markets.

Layered Detection Through Combined Processes

Synergies emerge when validation outputs feed directly into risk scoring engines that weigh inputs from several sources simultaneously rather than sequentially, allowing the system to adjust thresholds dynamically based on the combined signals. For instance, a successful AVS match paired with a new device fingerprint might still elevate the risk score if the transaction originates from a high-velocity corridor identified in recent network reports, and this integrated assessment occurs within milliseconds at the terminal gateway. Research compiled by organizations such as the Bank for International Settlements indicates that multi-national networks employing these coordinated scoring models record lower rates of disputed transactions across tested implementations.

Additional elevation occurs through the incorporation of tokenization services that replace sensitive card data with unique identifiers usable only within specific network segments, and these tokens carry metadata from prior validation steps that subsequent terminals can access. When a token travels from a European terminal to one in the Asia-Pacific region, the embedded history of checks performed earlier informs the local risk engine without requiring full re-validation of every element. This continuity reduces processing latency while preserving the cumulative protective effect of the original validation sequence, according to technical documentation released by standards bodies overseeing global payment interoperability.

Operational Implementation Across Borders

Terminal networks operating across jurisdictions must align validation configurations with varying regulatory mandates, including data residency rules and authentication requirements that differ by market, yet the underlying synergy mechanisms remain consistent through shared technical specifications. Processors deploy centralized policy engines that distribute updated rules to edge terminals, ensuring that a change in one region's validation priority propagates efficiently without disrupting operations elsewhere. Figures from industry monitoring groups reveal steady improvements in detection accuracy as these synchronized systems mature, particularly in corridors handling recurring or high-value transactions.

Training modules for network administrators emphasize recognition of how isolated validation failures can signal broader issues when viewed through the combined dataset, and simulation environments replicate cross-terminal scenarios to prepare teams for anomalies that span multiple countries. Such preparation supports consistent performance even as new terminal models and software versions roll out, maintaining the integrity of the layered detection framework through June 2026 and beyond.

Conclusion

The cumulative effect of interconnected account validation steps continues to define detection capabilities within multi-national terminal networks, where each component contributes context that strengthens the collective defense. Ongoing refinements in data exchange protocols and scoring algorithms support this integration as transaction environments evolve, providing operators with structured approaches to managing risk across expanding geographic footprints.